"Starbucks has become an everyday stop for millions.Trechos retirados de "Why ‘basic’ is bad for Starbucks".

.

But that ubiquity could now be its problem.

“Starbucks is now competing with chains like Dunkin’ Donuts and McDonald’s,” Business Insider proclaimed this week. “It has gotten, in a sense, too basic.”

...

So what’s an overexposed company to do?

Starbucks in recent years has begun looking for ways to restore its luster.

...

But can a brand that’s gone mainstream turn high-end again?

...

“I’ll just say this: It’s much harder to go up-market than it is to do the opposite,”

...

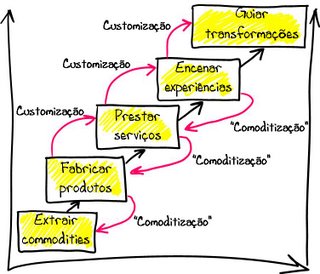

It’s a phenomenon Pam Danzinger calls “lux-flation”: Our ideas of what constitutes a premium product or experience are always evolving. “A brand like Starbucks starts at the top, and as it expands, it becomes the new normal,” said Danzinger, author of “Putting the Luxe Back in Luxury.” “Now it’s got to create that mystique once again.”

...

“They’re putting the human touch back into the equation,” Danzinger said. “That’s one way to regain that luxury edge.”[Moi ici: O oposto da Grab & Go, meter interacção, fugir da automatização]

...

But, he says, there have been some successes: In the early ’90s, Gucci was almost done for. [Moi ici: A propósito da Gucci, "De ajavardamento em ajavardamento] The Italian fashion company was in financial despair and its creative director was quoted as saying “no one would dream of wearing Gucci.” Then Tom Ford took over, and revived the brand, boosting sales and restoring the company to its previous glory.

.

“There are examples, but it takes a lot of money and a lot of paring back,” Pedraza said. “And frankly, not every company has the courage to do that. Everything is so grow, grow, grow in today’s world. And before you know it, you have a mainstream brand that isn’t special anymore.”"[Moi ici: Julgo que há aqui qualquer coisa metafórica acerca do fim do capitalismo dos últimos 200 anos. Quando se chega ao fim da rua e não há mais terreno novo para explorar, e já não há possibilidade de crescer como dantes]

Suspeito que no futuro me irei recordar muitas vezes deste texto "Hipsters and artists are the gentrifying foot soldiers of capitalism". Sobretudo deste trecho, tão ao modo de Mongo, tão ao modo de fechar o ciclo e voltar ao pré-Revolução Industrial:

"I asked the hipster owner and his beard-nurturing hipster customer (a tattooist from across the road) how they described themselves. “Socialists,” they replied, quickly adding that they were not looking “to build empires”, just to “make a living”. They had both left safe jobs working for the state and local government respectively. This led me to wonder about suggestions that the hipster may represent some form of reincarnated frontiersman/woman or pioneer. In many ways, I think they do. Their styling certainly harks back to the mid-to-late 19th century; to the British colonialists and the western frontiers. These people want to earn a reasonable living, independently, by “crafting” and “creating”. They, like the original pioneers, are explorers and artists and they are capitalists.

.

Unlike the colonising pioneer of the past, however, the hipster is postmodern, post-industrial, and post-Fordist."